Novated Lease - FBT Exempt EV's

All you need to know about FBT exempt Novated Leases on EV's.

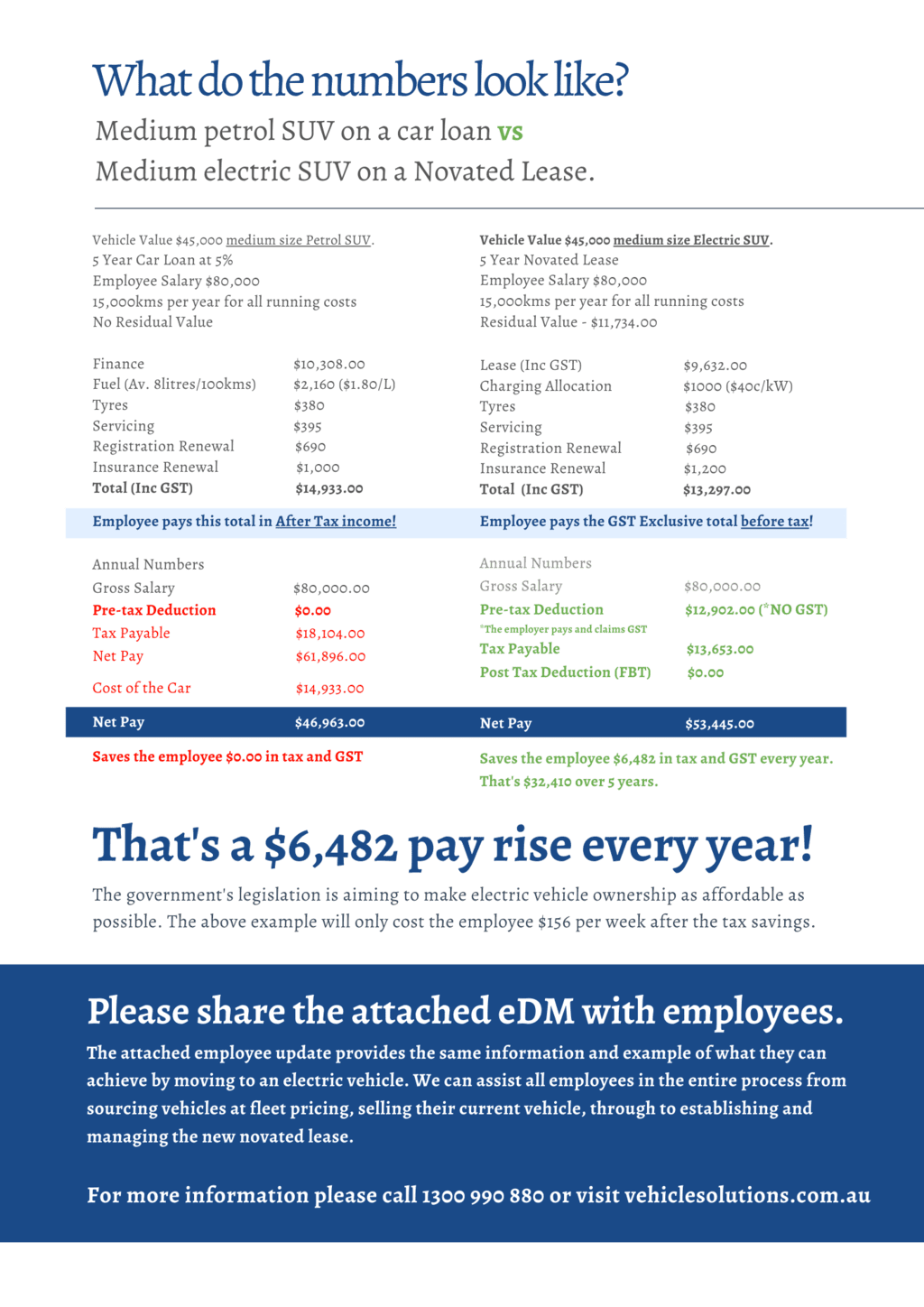

At the end of 2022 the Australian parliment passed an ammendment to the Tax Act making any Electric and PHEV under $84,916 FBT Exempt. The following sections from the ATO website provide accurate transparent information and clarity around the requirements in taking advantage of this incredible incentive to transition into an EV immediately.

Eligibility

You do not pay FBT if you provide private use of an electric car that meets all the following conditions:

- the car is a zero or low emissions vehicle

- the first time the car is both held and used is on or after 1 July 2022

- the car is used by a current employee or their associates (such as family members)

- luxury car tax (LCT) has never been payable on the importation or sale of the car.

Benefits provided under a salary packaging arrangement are included in the exemption.

The government will complete a review into this exemption by mid-2027 to consider electric car take-up. We will provide an update when this review begins.

What Vehicles are covered

Zero or low emissions vehicle

A vehicle is a zero or low emissions vehicle if it satisfies both of these conditions:

- It is a:

- battery electric vehicle

- hydrogen fuel cell electric vehicle, or

- plug-in hybrid electric vehicle.

- It is a car designed to carry a load of less than 1 tonne and fewer than 9 passengers (including the driver).

Motorcycles and scooters are not cars for FBT purposes and do not qualify for the exemption, even if they are electric.

Plug-in hybrid electric vehicles – 1 April 2025 onwards

From 1 April 2025, a plug-in hybrid electric vehicle will not be considered a zero or low emissions vehicle under FBT law.

However, you can continue to apply the exemption if both the following requirements are met:

- Use of the plug-in hybrid electric vehicle was exempt before 1 April 2025.

- You have a financially binding commitment to continue providing private use of the vehicle on and after 1 April 2025. For this purpose, any optional extension of the agreement is not considered binding.

For a full list of FBT Exempt EV's available in Australia now click HERE.

Are Used EV's FBT Exempt

'Held and used' the electric car

The practical effect of this requirement is that the electric car must be used for the first time on or after 1 July 2022 – even if it is held before this date.

An electric car is 'held' when it is:

- owned (includes cars acquired under hire-purchase arrangements)

- leased (or let on hire), or

- otherwise made available by another entity.

An electric car is considered 'used' when it is used or available for use by any entity or person.

Example: exemption does not apply – car first used before 1 July 2022

Shelly purchases an electric car on 1 April 2022. She makes it available for the private use of her employee, Jack, from that date until 30 July 2022.

On 1 August 2022, Shelly sells the electric car to ABC Co. ABC Co makes the car available for the private use of its employees from 1 August 2022.

The first time the electric car was both held and used is before 1 July 2022. Therefore, any car fringe benefits are not exempt from FBT.

For the ATO Fact sheet on EV FBT Exemption on Novated Leases please click here.

Thank you to the ATO for a majority of this information and for providing clarity on the changes to the tax act so quickly and efficiently.